Hello Eugene and everyone, this is my first message to the list, although I have been collecting data and trading with JBT over 2012 as well with various results (in general positive; I used the old long and short defenders and some own strategies). First, I would like to thank Eugene and the other contributors for the great platform that is JBT. Congratulations!!

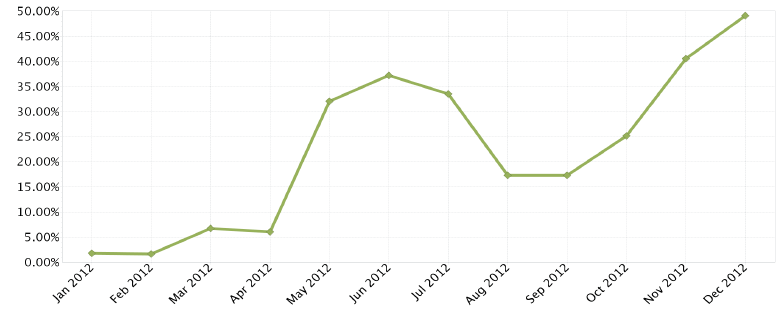

I would also like to start commenting a couple of simple ideas for which I would like to get your views: - It seems that the strategies work fine over a period of weeks following a certain market trend or market conditions. However, as JBT strategies are intraday, they do not take into account the overall trend of the last weeks. However, my experience is that they can be quite sensitive to it. For example, perhaps the platform could easily generate a file (from the logged data or from IB) with some daily values e.g. the open, close, max, min, volume, etc. so that strategies use this info when launched everyday e.g. to not enter (or control position sizing in the new version?). Maybe it goes a bit agains the JBT phylosophy, and maybe there are other ways to avoid entering in adverse periods, but I thought it was worth commenting... - Another idea not related to the above, and not even implying any change to JBT, would be to compile a sort of 'feared events' data set, or black swans if you like, including only days in which the market behaved weirdly, to backtest a strategy before launching. This is done often in safety systems engineering (which is more related to my background than futures trading!). Cheers, Inaki El martes, 1 de enero de 2013 19:42:39 UTC+1, nonlinear escribió: > > Hello JBTers, and happy new year! > > It's been relatively quiet in the JBT discussion forums, but for me > personally, a lot of things have happened: > > 1. Another JBookTrader version was released, which added to the stability > of the platform. > > 2. I traded with JBookTrader live, every day, methodically, and without > interference. It paid off, as my account returned 50%. I was trading 8 > strategies, 4 short-only, and 4 long-only. Each strategy is independent, > and trades 1 ES contract. The performance chart (from the IB report) is > below. > > 3. In 2013, I am scaling it up to 14 ES strategies, and starting to > accumulate the data for another instrument (the 30-yr bond US future). > > 4. Three months ago, I started tracking the performance of my IB account > with RapaCap, which is the service to match best traders with the capital. > Based on the short term tracking performance, I made it to the top 10 > traders: > http://rapacapintro.com/account/leaderboard/landingpage > My account is shown as nonlinear/JBookTrader in the leaderboard. > > 5. I am continuing to work on JBookTrader to improve its robustness, > features, and performance. Sometime in January, I'll release the next > version of JBookTrader, which would include: > a) improved performance of the "brute force" and the "divide-and-conquer" > optimizer > b) automated holiday detection > c) portfolio manager (for better handling position sizing when running > multiple strategies) > d) new performance metric > e) enhancement to trading schedule > f) re-subscription feature for long-running JBT sessions > g) other minor changes and improvements > > Feel free to share your success stories (and failure stories) with > JBookTrader in this thread. > Good luck to you all in 2013, > Eugene Kononov. > > > <https://lh4.googleusercontent.com/-Gz_jibyYJSg/UOMt0RjHOKI/AAAAAAAAADE/WZIQYCu2FEY/s1600/performance.png> > > > > -- You received this message because you are subscribed to the Google Groups "JBookTrader" group. To view this discussion on the web visit https://groups.google.com/d/msg/jbooktrader/-/4AryCz85L6QJ. To post to this group, send email to [email protected]. To unsubscribe from this group, send email to [email protected]. For more options, visit this group at http://groups.google.com/group/jbooktrader?hl=en.

{kind=link}